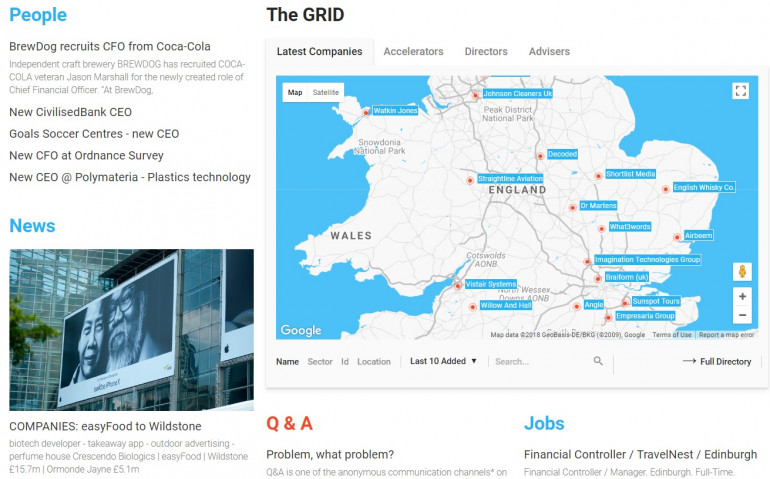

Published by Directorzone Markets Ltd on September 1, 2016, 9:00 am in Knowledge, Market Info

Wednesday January 1st 2020

Digest of news and trends in the GRID marketplace in August 2016:

Workplace Pensions | Supplier Contract Terms | Chinese UK Investment up 500% | Universities & Business | Cornwall Mining Revival | British Wine | L&G; -> VC | British Bioelectronics

WORKPLACE PENSIONS

The best way to build a Nest egg | Andrew Bounds, FT. August 29

…. research shows that almost all business people realise they must provide pensions. The final 1m small and microbusinesses, those with less than 50 staff, will have to sign up by early 2018. The rule applies to anyone aged between 22 and state pension age who earns more than £10,000 per year, though they may choose to opt out.

Some 206,000 employers have signed up 6.5m workers so far, according to the Pensions Regulator.

Many of the smallest businesses currently have limited choices, as some big providers do not want to deal with lots of little schemes. …it is as complicated for them to set up a pension plan for 10 employees as 10,000.

Some providers levy charges on the employers to establish a scheme, typically a few hundred pounds. After that it is usually free for the employer, but staff have to pay annual management fees of between 0.3 and 0.8 per cent of assets.

By April 2019, according to the Department for Work and Pensions (DWP), automatic enrolment into workplace pensions will generate £15bn in new pension savings every year.

So far roughly 30 insurers and 70 “master trusts” — who group multiple employer schemes together and funnel them to an insurer — have lined up to serve this market. But only seven of these providers will deal with the smallest employers.

NEST, the government provider…was set up to plug the pensions gap before the state decided to compel companies to do the job. It is free for SMEs and 100,000 use it, with more than 3.3m members, half the market. Nest charges just 0.3 per cent for its annual management fee, although it also levies 1.8 per cent on contributions. For now, Nest remains the safest pension option for workers and employers

SUPPLIER CONTRACT TERMS

Deals with big suppliers often turn sour, leading to calls for more protection | Kiki Loizou, The Sunday Times. August 21

Federation of Small Businesses (FSB) research showing that …More than half its members claim to have suffered as a result of supplier contract terms they feel are unfair, in sectors from communications and energy to financial services. Rollover clauses and lengthy notice periods are two common complaints. More than 40% of respondents say they feel unable to challenge contract terms because the supplier is too powerful.

The FSB estimates that such issues have cost Britain’s small companies a combined £4bn in the past three years. It wants the government to give them the same rights as consumers when negotiating with utilities and other suppliers.

CHINESE UK INVESTMENT UP 500%

Dean Kirby, inews. August 29

China’s investment in business and infrastructure in the UK has increased by almost 500 per cent in just the past six years, analysis has revealed. Chinese companies have splurged £3.8bn on 20 mergers and acquisitions so far this year compared with just nine deals worth £666m in 2010 – a rise of more than 470 per cent.

The Chinese have already pumped about £29bn into UK investment and contracts since 2005 and have taken a huge stake in the nation’s real estate, football clubs and household companies including Weetabix, according to separate figures from the American Enterprise Institute and the Heritage Foundation. The biggest draw for the Chinese has been real estate, with £9.5bn invested since 2005, followed by energy, finance and agriculture. Transport, metals, entertainment and technology have also received billions of Chinese cash. Technology and energy have had the biggest investments this year.

A 2014 report by international law firm Pinsent Masons and the Centre for Economic and Business Research also found that China is set to invest a “game-changing” sum of £105bn in UK infrastructure by 2025.

For China Inc, the most commonly practised strategy to invest in the UK is through merger and acquisition to targeted British companies. In doing so, it will ultimately increase the companies’ exposure to mature market economies, allowing them to learn sophisticated management skills and to create long-lasting brand value for their products. These intangible assets are abundant in the UK but relatively scarce in China.

The “investing in the UK” strategy is to diversify China’s enormous amount of foreign reserves and to underpin China’s currency value appreciation with the rest of the world.

UNIVERSITIES & BUSINESS

Universities build business links as funding dwindles | Helen Warrell, FT. August 19.

The value of commercial tie-ups between British universities and businesses has risen by more than 6 per cent to £4.2bn year on year, as higher education bodies seek out other ventures to compensate for leaner public funds.

….the Higher Education Funding Council for England (Hefce) statistics covering the collaborations between universities and businesses in 2014-15 compared with the previous year. These covered joint research — which increased by nearly 10 per cent to £1.3bn — to consultancy, involvement in continuing professional development programmes, and income from intellectual property, which rose by more than 18 per cent to £155m.

Hefce highlighted the fact that companies created from intellectual property developed in universities increased turnover and staffing by 138.6 per cent and 18.9 per cent respectively. There were also rises in the total number of graduate start-ups and social enterprises.

The new figures challenge the accusation that UK universities are less commercially adept than higher education rivals in the US and Asia: comparisons show that return on investment from commercialisation of research and engagement with industry are higher in the UK than in Japan and on a level with the US.

This is despite the UK investing just 1.7 per cent of GDP in research and development — well below the OECD average of 2.4 per cent.

CORNWALL MINING REVIVAL

Cornwall comes round to tin mine revival | James Wilson, FT. August 16.

South Crofty, the last Cornish tin mine to fall victim to a devastating price slump has been shut for almost two decades and … looks set for a rebirth. Strongbow Exploration could have the mine in production by 2019 or 2020, delivering 20 tons of tin a day. The mine’s revival, at an estimated cost of £100m, would be part of a renaissance in UK mining. International entrepreneurs, emboldened by the commodities boom of the past decade, have reappraised half-forgotten UK projects in light of better prices and new technology.

Last year an Australian company started to produce tungsten from an open-pit mine near Plymouth — the first new metals mine in the UK for more than four decades — and an Australian entrepreneur is leading a $2.9bn project to extract fertiliser from under the North Yorkshire moors.

Meanwhile an Ulster-born miner is behind a Canadian company’s attempts to build a gold mine amid the green hills of Northern Ireland.

Cornwall is an obvious place to share the revival. The county once dominated global supplies of copper and later tin, before the global tin price crash of the 1980s scuppered operations.

Frances Wall, professor of applied mineralogy, says there is scope for other resources to be developed, including the rare earth indium — “the material that allows us to make smartphone screens”.

BRITISH WINE

You need a lot of Yorkshire bottle to take on Bordeaux |Emma Broomfield, The Sunday Times.

For decades the British wine industry was considered a national embarrassment. However, its fortunes are on the rise. Last year there were 502 commercial vineyards and 133 wine producers registered in England and Wales, after 37 newcomers launched. More than 5,000 acres of the country are “under vine”, pushing production beyond 5m bottles year. However, that is a drop in a European Union wine lake compared with France, which produces 6.2bn bottles.

British wine exports should rise from £3.2m in 2015 to more than £30m by 2020, according to the Department for Environment, Food and Rural Affairs. But …. Small producers, in particular, must battle with the inconsistent climate and high production costs to make their businesses viable.

The burgeoning British wine industry is also expected to be heavily affected by Brexit. While the weak pound may have made UK winemakers’ exports more attractive, the long-term consequences are less clear as Britain may no longer benefit from free access to European markets.

L&G; -> VC

Legal & General to move into venture capital | Oliver Ralph, FT. August 10

Legal & General is to move into venture capital as it shifts from market-based investments to more direct ways of putting its money to work. “There’s a huge gap in the market,” said chief executive Nigel Wilson. “Universities in Britain are creating great science but there’s a shortage of capital. The UK is great at start-ups but awful at scale-ups.”

FT READER COMMENT, John Jones:

First, it's important to realise that organisations like Legal & General and the Prudential have long since stopped being simply insurers, as most people imagine them to be, and have become large-scale investors, in fact some of the very biggest institutional investors in the UK: for decades they've been putting all those premiums and other regular payments to work, generating a return both to meet the related liabilities and to make a margin for their shareholders.

Second, direct investment in income-generating assets isn't exactly terra incognita to these organisations: check the information on many big property developments in recent decades (shopping centres have been a particular favourite but also office blocks) and you'll often find that one of the big insurers like the Pru or else a pension fund is actually the owner.

Third, in an environment where returns on fixed income and on cash are so low, too much reliance on conventional fund management practice looks ever more unwise: getting more exposure to venture capital would not only allow insurers to capture some of the superior average returns available to investors in that sector but also be very good for the wider UK economy where access to investment has long been identified as a key obstacle to innovation and growth.

BRITISH BIOELECTRONICS

Google and GSK create a world leader in bioelectronics | Clive Cookson, FT. August 2

GlaxoSmithKline, Britain’s largest drug company, is teaming up with Alphabet, Google’s parent company, to invest £540m in bioelectronics at its global research centre in Stevenage. GSK is to set up a joint venture, GALVANI BIOELECTRONICS, with Alphabet’s life sciences subsidiary Verily, to treat disease by targeting the electrical signals passing along the body’s nerves rather than through chemical or biological drugs.

The partners plan to invest £540m over seven years in the jointly owned company, as well as contributing their existing intellectual property. GSK will own 55 per cent of Galvani and Alphabet the remaining 45 per cent.

Looking further ahead, Galvani puts the UK at the centre of what could become one of the mainstays of medicine in the mid-21st century, alongside conventional drugs and vaccines.

GSK already has around 50 bioelectronics collaborations with university teams and small biotech companies around the world. It has also put $50m into a specialist bioelectronics fund, Action Potential Venture Capital, which has invested in six start-up businesses.

Combine the Google empire’s expertise in miniaturisation, electronics, data analysis and software development with GSK’s experience in life sciences and clinical development — or Silicon Valley computing with British biology — and a world leader seems set to emerge.

Although the brain might seem the most obvious target for bioelectronics, neurological diseases are not the priority for Galvani. Rather than aiming at the central nervous system, the researchers are looking to intervene in the “peripheral nervous system” which plays a role in many chronic diseases, such as arthritis, diabetes and asthma.

Animal experiments have already shown that miniaturised electronic implants can have a beneficial effect on inflammatory, metabolic and hormonal disorders.

FT READER COMMENT, Occam:

Electrical messaging in the body makes use of small electrically charged molecules, or ions, which have a comparatively high mass and therefore high inertia, reducing reaction time of the system. Hence it takes about 1 second for an athlete to start moving his muscles as measured from the moment the start shot goes off. In classical electrical systems, the massaging is done via electrons moving through metal wires. Electrons have a negligible weight compared to atoms or molecules, hence lower inertia, hence much faster reaction times for the system. This is why a simple pocket calculator can calculate much faster than any human. Even faster are indeed photons (or electromagnetic waves) which technically are not particles, have 0 mass and move at the speed of light. If human bodies were using photons for information processing imagine all the things we could do in a lifetime.